-

Sector Focus

We specialise in the investment management industry offering audit, assurance, tax and corporate recovery and liquidation services.

-

Personal Tax Services

There are many tax rules that can affect you personally and therefore which will have an impact on your personal wealth.

-

QI Compliance

Qualified Intermediaries (QI) have to take action now to perform a Certification to the Internal Revenue Service (IRS).

-

Download our tax brochures

The tax teams at Grant Thornton aim to provide the Channel Islands with a premier tax advisory service both to private clients and the business community including the investment management industry.

-

Jersey Tax Return

A secure sign in page to file Jersey Tax Returns through the Grant Thornton tax portal.

-

ESG

ESG can either be seen as a risk management tool or an opportunity, either way it is imperative to your business, whatever your size and whether you are listed or not.

-

Professional Services

Business and accounting support for professional services

-

Finance Industry

We work with a broad range of clients and their financial stakeholders, from entrepreneurs in the early days to fast growing and established businesses to public companies competing in global markets.

-

Local Businesses

Businesses come in many shapes and sizes – from innovative start-ups to long-established local businesses. But however large or small your business, the chances are you face similar challenges.

-

Corporate Insolvency

Our corporate investigation, Guernsey liquidation and recovery teams focus on identifying and resolving issues affecting profitability, protecting enterprise value and facilitating a full recovery where possible.

-

Corporate Simplification

Redundant corporate entities can over complicate group structures and waste thousands of pounds in unnecessary costs each year. 46% of the c.15,500 companies controlled by the FTSE100 are dormant and it is estimated that the average cost of administering dormant companies is between £3,500 and £5,000 per company, per year.

-

Debt Advisory

Our Debt Advisory team provides commercial and financial debt advice to corporate entities and public sector bodies in a range of sectors. Our engagements include advice on stand-alone transactions and solutions or as part of an integrated business plan, in both the project and corporate arenas.

-

Exit Strategy Services

We offer a tailored methodology designed to enable a company to be reviewed in a group context to assess ways to maximise its value.

-

Financial Restructuring

For companies challenged by under-performance we work with management teams, shareholders, lenders and other stakeholders to implement financial restructuring solutions creating a stable platform for business turnaround.

-

Strategic performance reviews

Strategic performance reviews analyse the key drivers of performance improvement. Our specialists utilise a framework to evaluate financial and operational options and to identify solutions for businesses and their stakeholders.

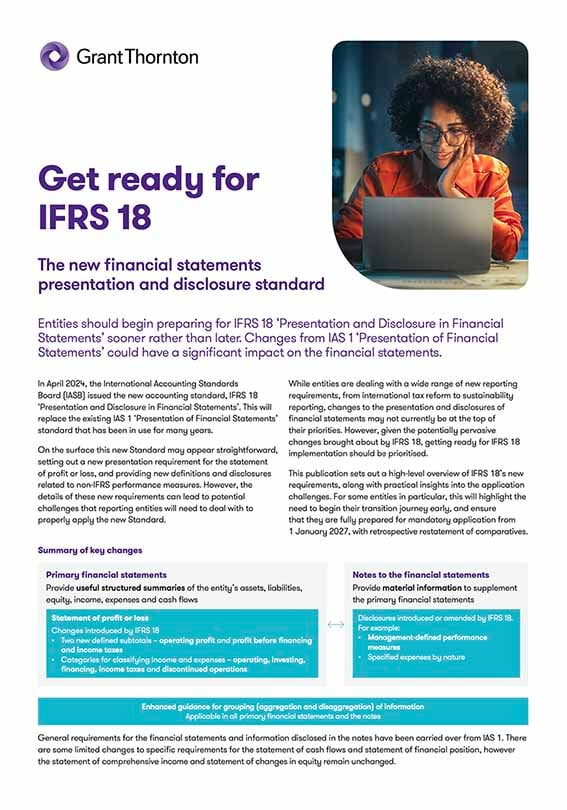

In April 2024, the International Accounting Standards Board (IASB) issued the new accounting standard, IFRS 18 ‘Presentation and Disclosure in Financial Statements’. This will replace the existing IAS 1 ‘Presentation of Financial Statements’ standard that has been in use for many years.

On the surface this new Standard may appear straightforward, setting out a new presentation requirement for the statement of profit or loss, and providing new definitions and disclosures related to non-IFRS performance measures. However, the details of these new requirements can lead to potential challenges that reporting entities will need to deal with to properly apply the new Standard.

While entities are dealing with a wide range of new reporting requirements, from international tax reform to sustainability reporting, changes to the presentation and disclosures of financial statements may not currently be at the top of their priorities. However, given the potentially pervasive changes brought about by IFRS 18, getting ready for IFRS 18 implementation should be prioritised.

Effective date and transition

IFRS 18 is effective for annual reporting periods beginning on or after 1 January 2027, with earlier application permitted. Entities that early adopt IFRS 18 are required to disclose that fact in the notes.

For some entities in particular, there's a need to begin the transition early to be fully prepared for mandatory application from 1 January 2027, with retrospective restatement of comparatives.

While IFRS 18 must be applied retrospectively applying IAS 8, entities are not required to disclose the quantitative information set out in IAS 8, ie entities do not have to disclose the amount of the adjustment to each financial statement line item or the adjustment to basic and diluted earnings per share in the current period.

For the comparative period, an entity must disclose a reconciliation between the restated amounts presented and the amounts previously presented for the comparative period applying IAS 1. This is also required for the comparative periods presented in interim financial statements prepared under IAS 34. Entities are permitted, but not required, to present similar reconciliations for the current period, as well as older comparative periods.

When first applying IFRS 18, an entity also has the option to change an election of how an investment in associate or joint venture is measured. If they are eligible to apply the exemption in IAS 28 ‘Investments in Associates and Joint Ventures’ (which applies for investments held by, or indirectly though, an entity that is a venture capital organisation, mutual fund, unit trust or similar entity), an entity may change its election for measuring investments from the equity method to fair value through profit or loss in accordance with IFRS 9.

How we can help

We hope you find the information in this article helpful in giving you some insight into aspects of IFRS 18. If you would like to discuss any of the points raised, please speak to your usual Grant Thornton contact.

Download Get ready for IFRS 18

This publication sets out a high-level overview of IFRS 18’s new requirements, along with practical insights into the application challenges.